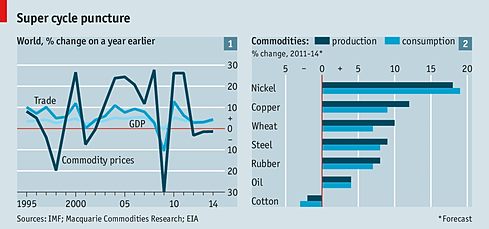

Between 2000 and 2011 broad indices of commodity prices tripled, easily outpacing global growth. Since the peak commodity prices have slumped by about a quarter.

Decreasing commodity prices are great news for net importers opposite to net exporters. Also consumers benefit from lower energy or agriculture product prices as they leave households with more disposable income.

Rising oil prices tend to push importing countries into recession. Also put pressure on currencies causing wider current account deficits. On the other hand commodity producing countries are generally poor and dropping prices damage their currencies and also negatively impact current account deficits. Generally speaking low commodity prices hit countries that relied on high ones.

In the short term commodity prices are a function of shifts in global demand expectations and interruptions in supply.

In 2008, the price of raw materials plummeted. Oil fell from $144 a barrel in the summer to $33 a barrel in December the same year. However, in 2010 the price was testing $100 again.

The current slide in commodity prices also reflects a weakening global world economy.

Both global GDP growth and trade have been decelerating since 2010. The WTO had forecast growth of 4.7% this year. Last September the figure was revised down to 3.1%.

Interestingly the WTO forecast a rebound in growth and trade next year. However, the 2000-2010 growth rates are very unlikely to repeat due to many risk factors like Russian expansionary policy (Crimea annexation, Eastern Ukraine invasion), Ebola virus spreading across Africa threatening the continent growth, terrorist and ISIL related problems, Hong Kong protests and democracy related ambitions contracting with the Chinese establishment interests.

Also the Eurozone which accounts for 13% of global output is playing with the recession zone. Growth looks extremely disappointing, inflation continues refusing to pick up, innovation and competitiveness levels look to be struggling against those of Asia and the U.S. On top of that the recent sanctions imposed on Russia will not help with the recovery Europe has been trying to achieve so much for sure.

China, which is one of the biggest commodity importers, is probably the biggest risk. China has been trying recently hard to shift its economy from manufacturing and raw materials consumption more towards stimulating domestic demand (local consumption), housing and infrastructure related projects.

On the other side of the globe we have America with oil production ambitions thanks to the recent fracking revolution.

As mentioned at the very beginning, production of most commodities has risen steeply over the past ten years. The global output of iron ore, for example, has grown three times since 2000! The biggest issue now is supply which is bigger now than demand causing the downward pressure on prices.

Emerging markets were a big driver of global GDP growth in recent years. The current negative commodity prices trend impacts severely commodity producers/exporters and will contribute to the global GDP growth slowdown.

However, some commodity exporters did their homework and look to be better equipped to manage the negative impact of the slowdown. Some of the countries managed to increase their foreign currency reserves or implement broader economic and structural reforms. The good examples are Colombia, Peru or Indonesia. On the other end of the scale we have Russia which heavily relies on oil and gas production. Although the central bank of Russia recently has spent the record amounts of U.S. Dollar to protect the ruble the local currency again hit the new low levels. The question is what’s the future for the economies like Russia once they run out of their natural resource? You need to have innovative and visionary leaders to assure the prosperous future of your nation regardless the moment of the commodity price super cycle.

Source: The Economist

Discussion

No comments yet.