By Jeffrey P. Snider, Alhambra Investment Partners

If China is most representative of the current state of the “dollar” economy, Brazil is surely most representative of its worst case. The country’s economy has been like China in slowing down steadily over the past few years, but unlike China it has descended already into a nightmarish level of distress. In other words, Brazil already has a Great Recession on its hands, only without the silver lining of a quick, symmetric recovery. Instead, they have a recession that only goes in the one direction, and holding that way for two years now.

If China is most representative of the current state of the “dollar” economy, Brazil is surely most representative of its worst case. The country’s economy has been like China in slowing down steadily over the past few years, but unlike China it has descended already into a nightmarish level of distress. In other words, Brazil already has a Great Recession on its hands, only without the silver lining of a quick, symmetric recovery. Instead, they have a recession that only goes in the one direction, and holding that way for two years now.

It is no wonder that its population is politically restive. For all the media attention to our own political discourse of late, Brazil is as its economic decay – amplified by that much more. The commonality of the unrest however manifested is poignant, as the people around the world are living in a world wholly different from what economists continue to describe, suggest and, for all of this, somehow still forecast.

Hundreds of thousands of Brazilians made a noisy and impassioned call on Sunday for the removal of President Dilma Rousseff, whose leftist government is plagued by a sprawling corruption scandal and an economic meltdown that has humbled Latin America’s largest country.

In times of economic growth, apathy usually allows for scandal and corruption as that is just human nature. We tend to focus on what directly affects our own standing, which is why sensitivity to politics noticeably rises during periods of great (and lasting) economic turmoil. That is true even if “the people” aren’t quite able to determine exactly what is causing the fundamental discrepancy.

“She’s a horror,” said Paulo Rodriguez, a 53-year-old businessman who came with his wife and daughter. “The Workers party is a horror. They’re a criminal organisation that is robbing state resources. They are destroying our country.”

Rodriguez’s primary frustration was with the economy. Sales at his crepe business were down 30% to 40% compared to last year, he said. Even though he believed opposition politicians were as crooked as those in government, he felt a change was needed.

“If Dilma goes, the currency will get stronger and confidence will return and people will start spending again,” he said.

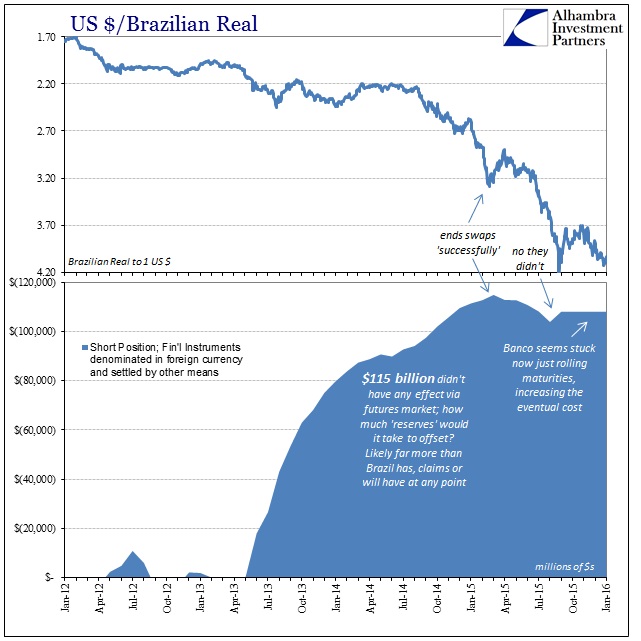

If only it were that easy. Such sentiment does, however, represent both hope and despair; hope in that the people of Brazil can see the agent of their own economic destruction, but despair in that they (quite reasonably) don’t know why that is. This has been the work of orthodox economics that has (often purposefully) spread and hardened into the dark of actual monetary function. It is the view of “reserves” as if they were anything like actual reserves, which is what economists have been suggesting for decades. It was conventional wisdom after the Asian flu that all that would be necessary to avoid serious economic and financial disruption was to carve out huge stockpiles of “reserves.”

Now, those countries with the hugest of stockpiles are those with the biggest (and most intractable) financial, “dollar” issues. Turning convention around in that way can only be mistaken assumptions about “reserves” in the first place. I wrote in August 2013 a post under a title I increasingly lament (Brazil May Already Be Toast) for its throwaway carelessness even though it describes the specific nature of modern, wholesale “reserves” and the Brazilian experience since. In other words,the nightmare scenario is that they are a misrepresentation and do not, in fact, provide salvation but rather, as China and many others are finding out, they become the rationale for undertaking the worst possible measures.

If we sum all of this up: the Brazilian central bank is aiding in the effort to short the real while the dollar will continue to rise against it as eurodollar funding markets process volatility driven by Bernanke’s attempt to undo the bubbles he finally sees as FOMC creations. I don’t see any realistic paths to how this will end well.

Central banks do not “calm markets”, they are the creators of instability in the first place. Any calm engineered by central bank intervention is as artificial as asset bubbles, and will get reversed in due course.

The greatest problem about the “global dollar short” is not the “dollar” part but the “short.” From that view, under these kinds of systemic circumstances, stockpiles of “reserves” are not that at all but rather an indirect indication of just how “short” a specific country or currency connection to the eurodollar system might be. It is not a source of strength but a partial indication of fragility. In Brazil, that might be the most literal truth as the manner in which the central bank uses its “reserves” suggests nothing like what is supposed to happen with foreign reserves.

The Banco’s “swaps”, then, act only on implied future dollar rates, increasing the cupom cambial (the onshore dollar rate implied by currency futures and spreads with dollar rates). In other words, since the central bank “swap” reduces the futures price of dollars in relative comparison to the spot price, there is a greater incentive for banks (both Brazilian and foreign) to borrow US dollars on foreign markets and import them to take advantage of the cupom cambial spread. The swap isn’t really a swap in the conventional sense since the central bank is only swapping dollar indexed securities – deliverable in reals. In short, it is the old central bank axiom of getting the “market” to do your dirty work for you.

Another way to succinctly describe what Banco had done is to write that it pushed banks in Brazil to go more short the “dollar” just ahead of the systemic (short) squeeze of the “rising dollar” period. Brazil is now paying for both the systemic “short” to begin with plus the added charge of the grave monetary mistake. Furthermore, it is still committing the economic larceny.

The fact that unrest is spreading and enlarging is a good thing if it becomes quickly enough a true search for cause; an actual accounting of “how” and “why” rather than the excuses for more political retribution from whatever “side.” History, however, does not suggest even that process to be painless and smooth, and that more often than not lingering economic disfavor becomes increasingly violent and socially destabilizing (even the US, civilized as we often find ourselves, has never been completely free from these passions). To state the obvious, there is a lot at stake.

And Janet Yellen is still claiming the recovery remains on track.

Discussion

No comments yet.