By Etienne Lepers

While Turkey – with its ceaselessly falling currency – is struggling with the same global forces as other emerging markets, an internal struggle between President Erdoğan, Central Bank Govenor Erdem and deputy PM for the economy Ali Babacan is undermining Turkish economic vitality. Interest and currency rates have become subject to inter-departmental feuding generating significant financial uncertainty.

While Turkey – with its ceaselessly falling currency – is struggling with the same global forces as other emerging markets, an internal struggle between President Erdoğan, Central Bank Govenor Erdem and deputy PM for the economy Ali Babacan is undermining Turkish economic vitality. Interest and currency rates have become subject to inter-departmental feuding generating significant financial uncertainty.

Over the past few years, the Turkish Lira – like many other emerging market currencies – has been facing global headwinds stemming from the U.S Federal Reserve tapering its quantitative easing program.

The Lira has fallen once again to record lows, now traded at around 2.6 against the greenback at the end of March (see chart below). All emerging countries (more or less) face the same dilemma: raise rates to stabilize their falling currency and their debt or ease rates to boost their growth rates.

Adopting this global perspective can be misleading, however, if it overlooks nation-level specifics. For instance, China has a unique set of conflicting economic goals that require ever more careful moves.

In Turkey, internal political disputes rather than economic choices determine the outcomes for interest, currency, and growth rates. In particular, investors need to consider the longstanding and evolving fight between President Erdoğan and Central Bank governor Erdam Basci.

Hold on Tight Technocrats

The dilemma highlighted above is due – on the one hand – to technocrats willing to adopt tighter monetary policies to stabilize the falling lira, smooth credit growth, and soften the current account deficit; and on the other hand, the President who wants to push Turkey’s economy to a target growth rate of 5%.

This battle of wills has led to mounting financial uncertainty in Turkey.

President Erdoğan is trying to strengthen his new presidential powers (which he received in mid-2014), simultaneously seeking to turn the country into a presidential system and to boost economic growth ahead of general elections in June.

In doing so, he has repeatedly lambasted the central bank’s independence, relying on his traditional anti-western/anti-Gülen/conspiracy theory rhetoric: Mr.Basci is accused of being a “traitor”, part of the “interest rate lobby” and controlled by “foreign interests.”

Moreover, high interest rates are said to increase inflation – in a complete denial of economic theory –, to make the country “impossible to invest [in]”, and are equated to “selling out the homeland.”

Each successive speech by the President espousing such views has been met with an instant weakening of the Lira. In the words of economist Dani Rodrik – “as [Erdoğan’s] power has increased so has his hubris and there are now very few people around him who dare to speak the truth about what is happening in the economy and to argue that his economic theory is nonsense.”

Opposing Erdoğan is Central Bank governor Erdem Basci, as well as deputy prime minister for the economy Ali Babacan. Tellingly, both men claim to “have the ear of Prime Minister Davutoglu”, and both admit to viewing their jobs as “damage control.”

How Does This Fight Over Monetary Policy Affect the Economy?

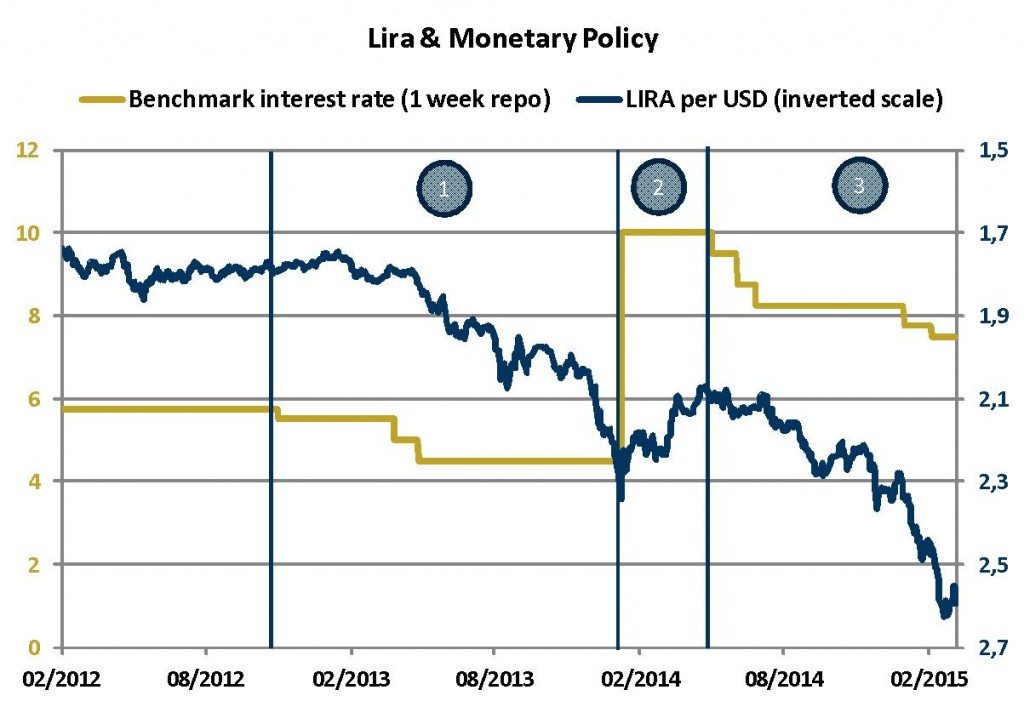

A simple chart can show the striking effect of the changes in monetary policy on the exchange rate:

The benchmark rate – in Turkey the one week repo rate – has already been decreased three times between 2012 and 2013, leading to massive capital outflows and the fall of the Lira (Period 1).

Govenor Basci had at that time responded aggressively by raising the rate from 4,5 to 10%, allowing the currency to strengthen for a while against the dollar (Period 2). From mid-2014, the constant pressures from Erdoğan to decrease the interest rates led (without apparent economic justification) to a series of five cuts (Period 3).

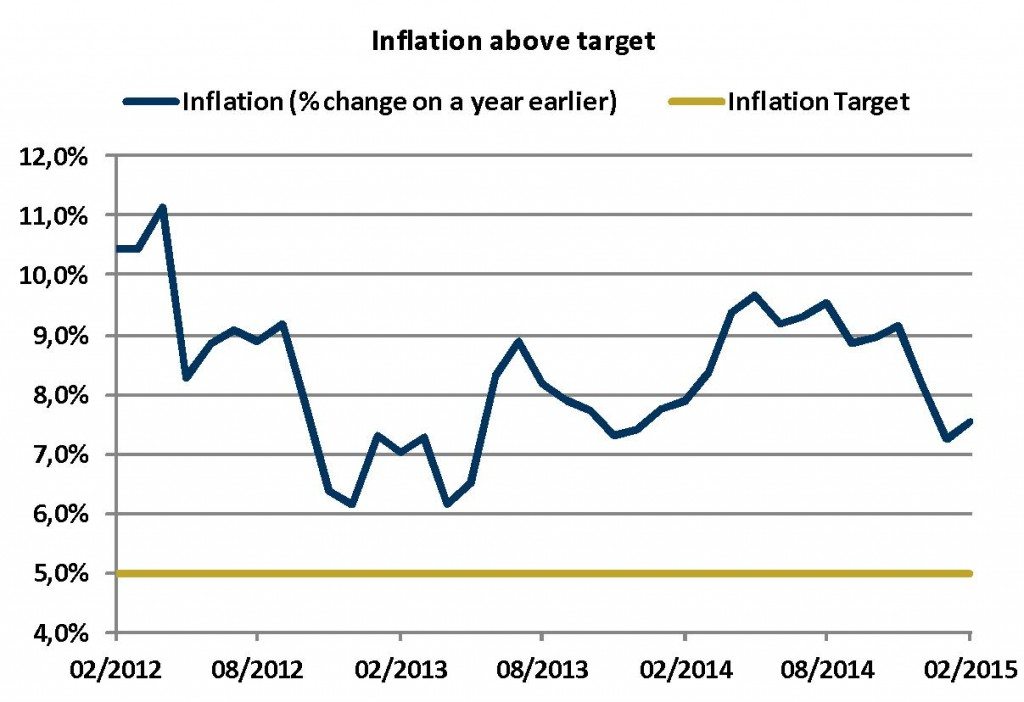

These moves occurred, despite inflation being well above set targets, (see chart below) and a high current account deficit – even though as a big energy importer, the falling oil prices should have improved both indicators. The consequences, however, have been clear, with the Lira sliding to record lows and investors fleeing: highly detrimental for an economy largely dependent on capital inflows.

Financial Uncertainty Continues in Turkey

Going forward, geopolitical tensions will push the Lira further down, as was the case in late March following the Saudi-led intervention in Yemen. Additionally, U.S. interest rates are expected to rise by mid year. Still, the U.S. rate rise having likely already been priced in the exchange rate market, and geopolitical risk has a comparatively small effect on the Lira.

External factors aside, the outcome will depend on Turkey’s internal political dynamic.

Recent events point to a lull in tensions between Mr. Basci and Erdoğan. They held a conciliatory meeting on 12 March.

Whether because or in spite of said meeting, the fact remains that the Central Bank has been able to resist further easing. Furthermore, the Central Bank has been able to maintain the same interest rates in the face of “uncertainty in global markets and elevated food prices.” The potential respite – if any – should not last long.

In June, Turkey will hold general elections, increasing uncertainty during both the pre- and post-election periods. Prior to the election, easing pressure on the central bank will give a temporary boost to the economy. After the election, newspapers will likely already be talking about the possible resignation of Mr Babacan or Basci.

The replacement of the current economic team with one that is more pro-growth – and less concerned about price and financial stability – would be a worrying perspective indeed.

In general there has, for a number of years, been a shift underway in Turkey towards a more presidential system. Such a system portends greater pressure on the rule of law as well as more disdain for cautious economic policy, thus leading to more political risk and less credible policies. And that is why technocrats should hold on tight.

Discussion

No comments yet.